[ad_1]

Reserve Bank of India Governor Shaktikanta Das on the RBI workplace, in New Delhi (Express Photo/Tashi Tobgyal/File)

Reserve Bank of India Governor Shaktikanta Das on the RBI workplace, in New Delhi (Express Photo/Tashi Tobgyal/File)

Dear Readers,

Exactly a 12 months in the past, Finance Minister Nirmala Sitharaman was requested if India was going through stagflation, which refers to a section when an economic system witnesses ‘stag’nant growth and persistently high in’flation’.

The query was requested as a result of India’s growth price within the first two quarters of the final monetary 12 months (2019-20) had decelerated sharply to a six-year low and retail inflation — or the speed of improve in costs that we face as customers — had shot up in November 2019.

She had reportedly replied: “I have heard of the narrative going on and I have no comments to make”. To be honest, on the time, calls of stagflation had been fairly untimely.

For one, retail inflation had gone up for simply a few months. Moreover, the primary culprits had been meals costs, particularly fruits and vegetable costs, which had shot up after unseasonal rains curtailed provides.

It was hoped that earlier than lengthy, the “transient” spike in inflation will subside and the GDP growth will resume momentum.

But neither occurred.

GDP growth continued to falter — it stored getting slower within the third and fourth quarter earlier than Covid compelled it to contract by 24% and seven.5%, respectively, within the first two quarters of the present monetary 12 months (2020-21).

The price of Inflation remained persistently high till Covid disruption made it worse.

📣 Follow Express Explained on Telegram

This brings us to the troubles of India’s central financial institution — the Reserve Bank of India — which launched its newest bi-monthly assessment of financial coverage final week.

The RBI is, by legislation, required to keep the retail inflation price inside a band of two% and 6%. At the beginning of the Covid breakout in late March and once more in end-May, the RBI furiously reduce rates of interest in order to increase financial exercise, whereas largely ignoring the hardening retail inflation price. Governor Shaktikanta Das made it amply clear that the RBI will do every part in its energy to revive growth.

But within the final three coverage critiques, together with the most recent one, the Monetary Policy Committee of the RBI has determined to hold the benchmark coverage rate of interest — the repo price or the rate of interest at which it lends cash to banks — unchanged.

For those that observe financial coverage intently, this resolution was a foregone conclusion even earlier than the RBI introduced it.

Why?

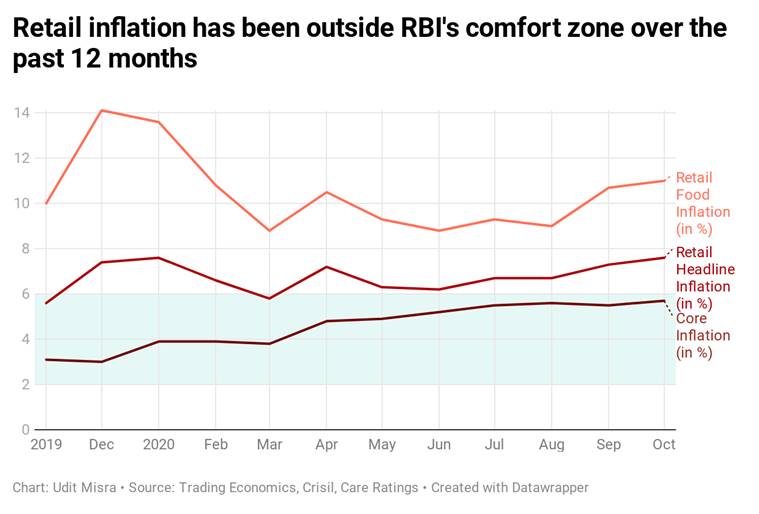

Because regardless that India’s economic system is struggling to develop, the retail inflation price — calculated utilizing Consumer Price Index — had remained above RBI consolation zone for nearly each month since final November (see Chart 1).

Before the December Four coverage announcement, most individuals believed — very like in November and December final 12 months — that it’s only a matter of time that retail inflation will come down, and when it does, the RBI will restart slicing rates of interest to increase financial exercise.

But right here lies a very powerful takeaway from the most recent financial coverage assessment: At lengthy final, the RBI admits that, removed from easing up, the inflation outlook is getting worse. “The outlook for inflation has turned adverse relative to expectations in the last two months,” said the coverage assertion. As a consequence, the RBI has considerably raised its inflation forecast not only for the present quarter (October to December) but additionally for the 2 quarters after this one — January to March and April to June in 2021.

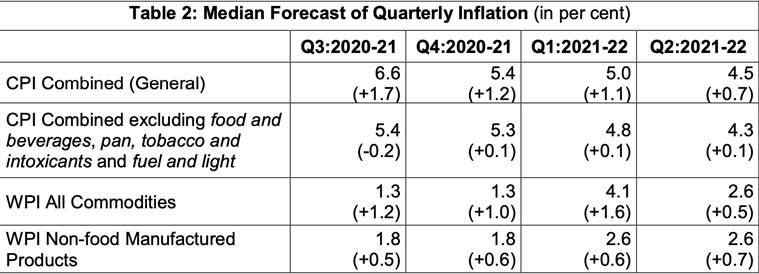

Look at Table 2. It is taken from RBI’s newest “survey of professional forecasters on macroeconomic indicators”. The figures in parenthesis present the extent of revisions. As will be seen by a sea of plus indicators, forecasters have bumped up inflation forecasts throughout the board — be it retail or wholesale, headline or core, this quarter or two quarters therefore.

Also in Explained: Gold costs now down, however does it make sense to keep invested?

Data is taken from RBI’s newest “survey of professional forecasters on macroeconomic indicators”.

Data is taken from RBI’s newest “survey of professional forecasters on macroeconomic indicators”.

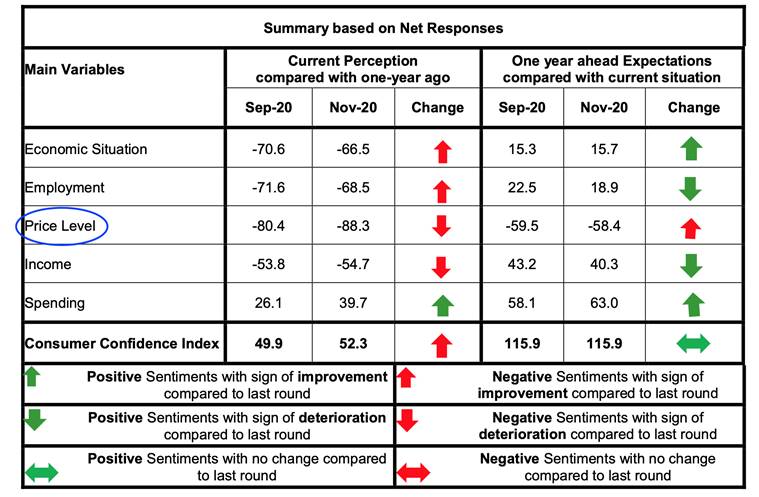

Table 3, which is taken from RBI newest “Consumer Confidence Survey”, is sort of revealing too because it exhibits that, within the 12 months forward, customers are optimistic about each macroeconomic variable barring the problem of costs.

Data is taken from RBI newest “Consumer Confidence Survey”

Data is taken from RBI newest “Consumer Confidence Survey”

The upshot of RBI’s evaluation of the economic system was that whereas growth is recovering, it isn’t as broad-based, and inflation is rising and it’s turning into extra broad-based.

The query a few of it’s possible you’ll justifiably ask is: Why hasn’t the RBI raised rates of interest? Isn’t it certain by legislation to keep worth stability?

This is a sound question. After all, if one seems to be at Chart 1, it’s clear that over the previous 12 months not solely has the headline inflation price been outdoors RBI’s consolation zone but additionally meals inflation has routinely touched double digits. Worst of all, even the core inflation price — or the inflation price after excluding meals and gas costs (each of which fluctuate quite a bit) — has continued to climb all by means of the 12 months and is now threatening to breach the degrees set for headline inflation.

Retail inflation has been outdoors RBI’s consolation zone over the 12 months

Retail inflation has been outdoors RBI’s consolation zone over the 12 months

An enormous a part of the reply to this query lies in understanding the explanation why inflation is high in India and whether or not elevating repo charges is the answer to that. As the RBI notes, the continuing inflation spiral is being fuelled by provide chain disruptions, extreme margins and oblique taxes.

For occasion, if the gas costs are increased as a result of the federal government retains elevating oblique taxes on them, then how far will a repo price improve carry down gas costs?

Similarly, if the value of an excellent is increased immediately as a result of the provision of products is disrupted thanks to Covid, can elevating repo charges carry down costs?

If the reason for the present inflation spike was extreme demand — “too much money chasing too few goods” — then elevating rates of interest may have helped issues. Higher rates of interest would have weaned off a ample variety of individuals away from spending and into investing thus bringing down the value stage.

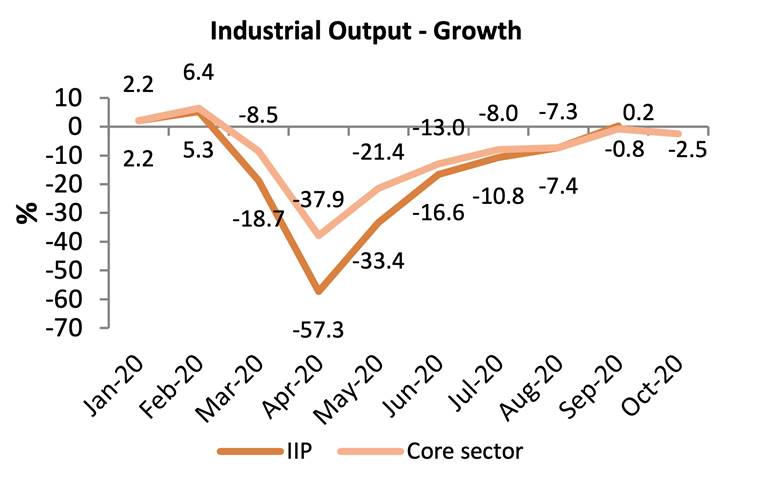

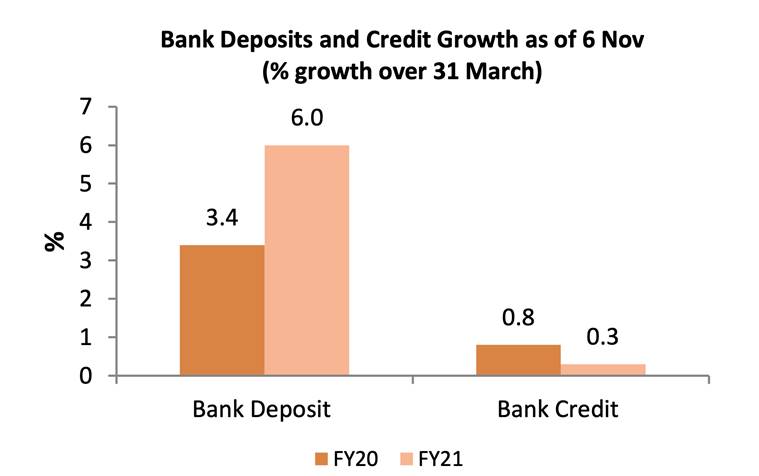

But that’s not occurring at current. Industrial growth is sort of non-existent (see Chart 4) and credit score off-take is anemic (see Chart 5). Capacity utilisation in corporations is low and they’re shedding staff to reduce prices.

Don’t miss from Explained: Why RBI has requested HDFC Bank to cease digital launches, new bank card sourcing

Industrial growth is sort of non-existent

Industrial growth is sort of non-existent

Moreover even elevating repo charges or slicing them usually takes a while — at the very least 1 / 4 — earlier than influencing the market rates of interest that you simply and I receives a commission.

That is why central banks are extra bothered about managing individuals’s expectations of future inflation as an alternative of reacting to month-to-month inflation actions.

If elevating rates of interest shouldn’t be efficient, then what’s the method to calm down costs?

Credit off-take is anemic

Credit off-take is anemic

The RBI underscores the necessity for “proactive supply management strategies. “Further efforts are necessary to mitigate supply-side driven inflation pressures,” it states.

Who will do that? Of course, the federal government. The RBI is already doing one of the best it may well — not elevating rates of interest even when all forms of inflation parameters are off the charts.

A 12 months down the road, India nonetheless can’t be characterised as going through stagflation. While GDP growth is anticipated to rebound, persistently high inflation is now turning into a fear that can not be brushed apart as seasonal or transient.

Stay protected,

Udit

An Expert Explains: Nature of financial restoration in India

© IE Online Media Services Pvt Ltd

[ad_2]

Source hyperlink

{kind=link}